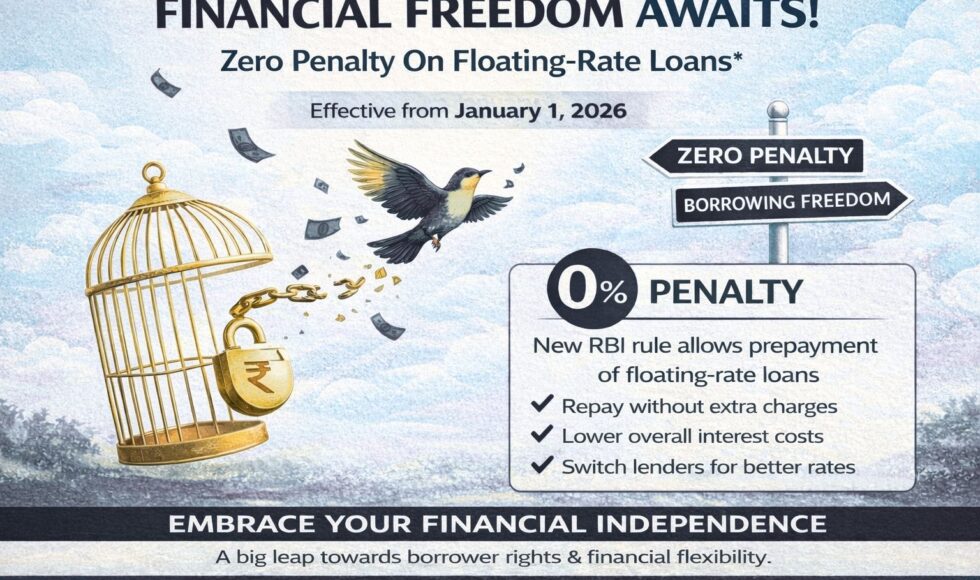

Effective from January 1, 2026

The Reserve Bank of India (RBI) has introduced a significant regulatory reform aimed at strengthening borrower rights and improving transparency in the lending ecosystem. Effective January 1, 2026, banks and Non-Banking Financial Companies (NBFCs) will no longer be permitted to levy prepayment or foreclosure charges on most floating-rate loans extended to individuals and Micro, Small and Medium Enterprises (MSMEs).

This move marks an important step toward making loan repayment more flexible, cost-efficient, and borrower-centric.

Understanding the New RBI Regulation

Under the revised guidelines, lenders are prohibited from charging any penalty when a borrower chooses to:

Make partial prepayments, or

Foreclose (fully repay) an eligible floating-rate loan before the end of its tenure

This applies regardless of whether the prepayment is made from the borrower’s own funds or through refinancing with another lender.

Scope and Applicability

The regulation applies to floating-rate loans availed by:

Individuals

MSMEs / Small businesses

Covered loan categories include:

Home Loans

Personal Loans

Vehicle Loans

Education Loans

Other floating-rate personal and business loans

The objective is to ensure borrowers are not financially penalized for responsible repayment behavior or for seeking better interest rates elsewhere.

Key Benefits for Borrowers

This regulatory change delivers multiple advantages:

Zero prepayment penalty – borrowers can repay loans early without additional costs

Lower total interest outflow over the loan tenure

Greater flexibility to manage surplus funds efficiently

Simpler loan switching to lenders offering better interest rates or terms

Enhanced transparency and fairness in loan agreements

Overall, borrowers gain stronger control over their financial planning and debt management strategies.

Illustrative Example

Consider the following scenario:

Total Loan Amount: ₹50 Lakhs

Outstanding Balance at Prepayment: ₹30 Lakhs

Earlier (Old Rule):

Prepayment charges (approx. 2%) = ₹60,000

Now (New Rule):

Prepayment charges = ₹0

✅ Direct saving of ₹60,000, along with reduced future interest costs.

Important Clarifications

The regulation applies to most banks and NBFCs operating in India.

Certain limited exceptions may exist for select co-operative banks, small banks, or specific loan categories (generally loans up to ₹50 lakh).

Borrowers are advised to review their loan agreements or consult their lender for exact applicability.

What This Means in Practice

If you have a floating-rate loan that is sanctioned on or after January 1, 2026, you can:

Repay partially or fully at any stage

Switch lenders without penalty

Reduce long-term borrowing costs

All without worrying about hidden prepayment or foreclosure charges.

Conclusion

The RBI’s decision reinforces its commitment to borrower protection, transparency, and financial empowerment. By eliminating prepayment penalties on floating-rate loans, this reform encourages healthy competition among lenders and enables borrowers to make smarter, more informed financial decisions.